Most serious students of the financial markets know that estimating asset returns is difficult. And while forecasting volatility is not easy, it is generally easier to estimate future volatility than to estimate returns. One reason is that volatility is not price directional. Volatility can be high regardless of whether prices rise or fall. Another reason is that volatility is serially correlated. If volatility is high today, it is likely to be high tomorrow and if volatility is low today, it is likely to be low tomorrow. This makes volatility trading potentially more lucrative than going long or short assets based upon a prediction of the price returns of the asset.

However, going long or short a single asset (such as stocks, bonds or a cryptocurrency), in an attempt to take advantage of volatility, does not work. If a trader believes that ETH will be more volatile in the next month, the trader may want to go long an ETH perpetual future. If ETH rises significantly, the trader makes money. But if ETH should decline significantly the trader would lose money. The trader could be right that the volatility of ETH increased but still make a loss if the trader fails to also correctly predict the price direction of ETH.

What is needed are investments that have little or no directional exposure to ETH but will profit from high or low volatility. Options are a type of instrument called a contingent claim that can be used for this purpose.

Condors

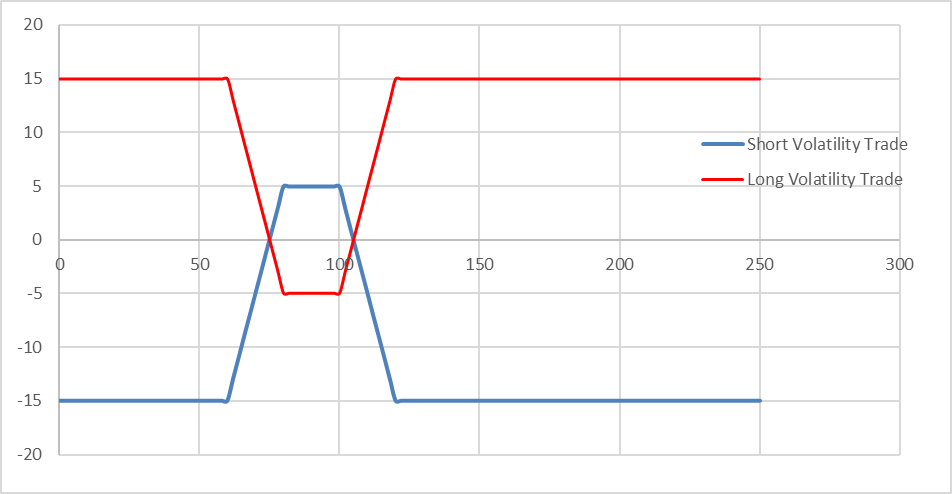

Combinations of options, exposure to the underlying and cash can be used to construct investments that have a variety of profiles and exposures. Below is a graph of a combination of puts and calls called a condor. A condor uses four options, a put spread and a call spread to create this profile. This same value profile can also be created by using four different calls or four different puts.

Condors that are long volatility are a combination of options that make money when volatility increases (the red line above), while the opposite option positions will make money in a low volatility environment (the blue line above). The expiration dates for all of the options in these trades are the same for collateral and risk reasons. Using spreads allows the trader to get exposure to volatility (long or short) while limiting potential losses to a value known to the trader at the time the trade is bought or sold. The maximum gains and losses are not only known in advance but the trader can adjust the exposure to the positions by choosing different option strikes to increase the potential gain (and increase the potential loss) or reduce the potential loss (and reduce the potential gain). The conder also need not be symmetrical. The largest potential gains can be targeted to be on either side of the current underlying crypto price. Another limited loss options combination that creates profiles like condors are butterfly spreads that once again use four options of the same type (puts or calls) with the same expiration date.

The advantage of these option spreads are that the potential losses if the change in volatility goes against the trader are limited. But these spreads also reduce the size of the potential gain.

Straddles & Strangles

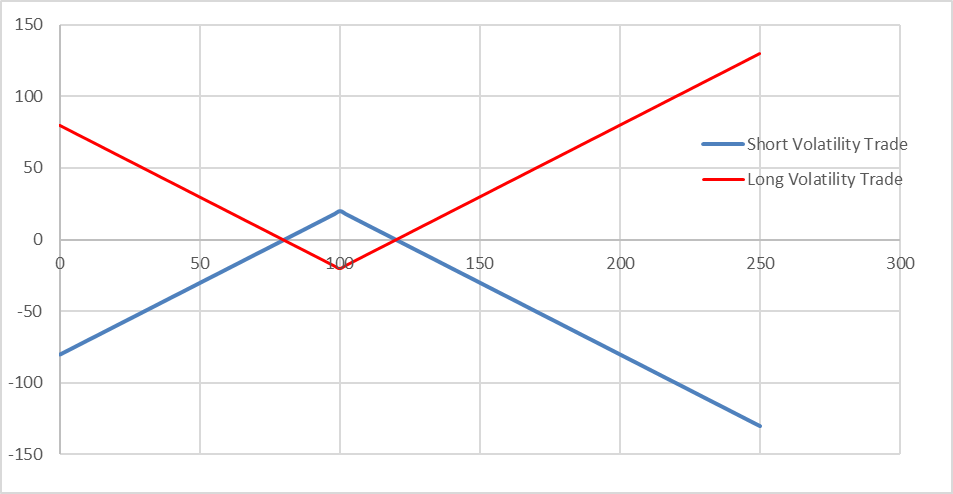

If the trader is more of a risk taker they can convert the condors into straddles or strangles. These trades consist of only two options instead of four options The long volatility trade consists of a long call and put. The short trade sells a call and a put. The strike prices of the options for straddles are the same for the call and the put. The graph below shows the payoff profile for long and short straddles (both put and call strikes are the same). Since the long volatility trades are long both a put and a call the trader will make money on the put until the underlying cryptocurrency hits $0. But on the long side there is no cap if the cryptocurrency advances. For the short volatility trader the maximum loss on the put is capped when the crypto currency get to $0 but the loss can be unlimited if the cryptocurrency moves higher.

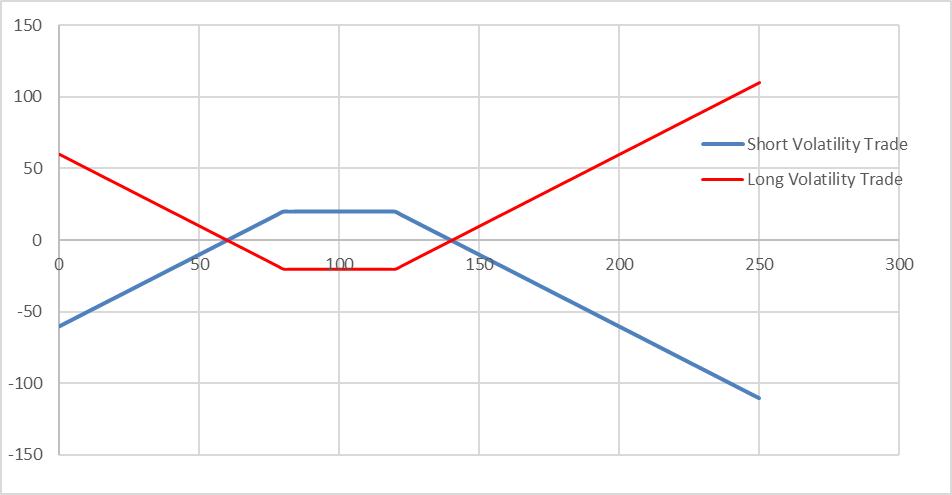

A variation of the straddle is the strangle. It is similar to the straddle but instead of the put and the call having the same strike, the strikes are split. This increases the area of a gain at the expense of less return. For strangles the put strike is below the call strike price. Strangles will be generally cheaper than straddles with the same time to expiration.

Compared to condors:

Straddles/strangles are more expensive but offer significantly larger potential gains

Long volatility positions profit on either extreme price movement

Short volatility trades may have unlimited loss potential if the underlying asset moves dramatically higher

Advanced Volatility Trading Strategies

There are other trading strategies used by professional traders to gain long or short exposure to volatility with negligible directional exposure. These include strategies such as volatility arbitrage, delta and gamma hedging and dispersion trading.

Volatility Arbitrage

Volatility arbitrage is misnamed in that it is not a true arbitrage where the gain is riskless. It involves buying or selling options based on perceived mispricing in implied volatility and hedging away the market exposure in the underlying using futures (or cash and underlying if futures are not available).

The most important factor in option pricing is expected volatility that is impounded in actual option prices. This expected volatility is called implied volatility. Volatility arbitrage involves the following process:

The volatility trader first estimates future volatility of the underlying asset such as ETH

They then compare that forecast to the implied volatility in options on ETH.

If the implied volatility in ETH options is higher than the forecast volatility of ETH, the trader sells a “overpriced” option or an “overpriced” collection of options such as a strangle or straddle.

If implied volatility is below forecast (underpriced options), buys options

The issue however is that a single option or strangles and straddles have directional exposure to ETH. Professional traders in this space will try to hedge away this exposure by delta hedging.

Delta Hedging

Delta is the underlying asset exposure represented in a single option or a collection of options. For instance, option positions with a delta of 0.36 are effectively long 0.36 shares of the underlying in addition to the volatility exposure (known as vega) in the options. A delta of -0.65 means that the option positions have an effective short position of -0.65 share of the underlying. Delta hedging this exposure means buying or selling the equivalent number of futures with the opposite sign against the option positions that are hedged. For instance if a volatility arbitrageur has short ETH option positions with a calculated delta of -0.36 the trader will offset that exposure by buying 0.36 ETH futures.

At-the-money options typically have deltas around 0.50 or -0.50, while deep in-the-money calls approach a delta of 1.0, and deep out-of-the-money calls approach 0. Understanding these relationships is crucial for implementing effective hedging strategies.

Volatility strategies that require delta hedging are risky. An accurate estimate of delta requires an accurate estimate of future volatility. An inaccurate estimate of delta results in the buying or selling of the wrong number of futures against the option positions used to profit from volatility. Delta hedging requires that the futures position be adjusted frequently so as to offset the effective underlying ETH exposure. But trading can be costly, reducing the profits from the volatility positions.

Dispersion Trading

Dispersion trading uses the principle that a diversified portfolio of cryptocurrencies are less volatile than a single currency position. This is because the portfolio of crypto currencies are likely relatively uncorrelated. This means that when some members of the portfolio go up others might go down. The higher the expected dispersion the lower the expected volatility of the underlying portfolio.

Implementation generally exploits the fact that the implied volatility of index options implicitly includes an expected correlation matrix for the component stocks. If dispersion is expected to be higher than expected dispersion in index options the trader would buy the individual stock options on the components of an index and sell the index options on that same index.

Obviously dispersion trading is not a true arbitrage but a trade that once again relies on an accurate forecast of the future correlation matrix. One advantage over delta hedged strategies is that the dispersion trade does not require frequent rebalancing.

Conclusion

Volatility trading and arbitrage can be exploited in a number of ways. Some with limited risk , some with unlimited risk and some that require frequent rebalancing and close monitoring. The choice of what method to use will depend upon the skill and knowledge level of the trader and the trader's risk appetite. Understanding these approaches allows traders to capitalize on volatility movements regardless of market direction.